Day 0 Account Value: $2500 (+$0/0%)

After all of our preparation and research, today was the day I laid out the first trades of our little experiment, selling iron condors on GLD (gold ETF) and TLT (U.S. Treasury Bonds ETF). I’ll walk through the thought process for only the TLT iron condor as the GLD spread followed similar logic. After open and into the afternoon, I had charts for each of our Top 10 underlyings open in the template I described in the previous post and examined volatility. For each of the ten, I asked the following: is implied volatility high, low or mid-range compared to itself, and is there a strong divergence or convergence of implied and historical volatility?

For the equity index ETFs SPY, QQQ, and IWM, implied volatility is mid-range and 3-4% above 45-day historical volatility. For now, I’m not finding that particularly interesting and I’ll pass.

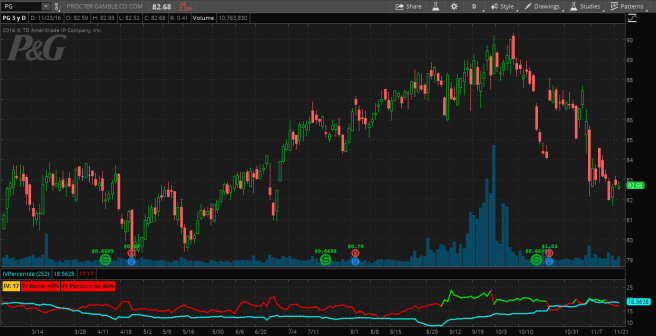

For our equity picks — AAPL, PG, BAC, FB, and BABA — implied volatility looks depressed (save PG at 60th percentile), but across the board is tracking historical volatility much tighter. An IV/HV spread of 1.1% on FB, for example, doesn’t give us much of an edge buying or selling volatility without trying to be predictive of the future. Keeping in line with our 30-60 day optimal expiry range, we’ll be looking at the Jan ’17 monthly options.

That left just two ETFs, GLD and TLT. Let’s examine the TLT setup:

At the time the trade was put on, TLT was trading with a 89th percentile IV and a 1.7% IV premium over HV. IV is certainly inflated compared to itself, but what about that IV/HV differential? Until I find a clean way to compare HV to itself, I have to rely on qualitatively interpreting the HV (blue) graph. A quick glance shows that HV is nearly as high as its been over the past year. With both IV and HV near the top of their ranges, I’m inclined to believe both will trend down towards their long-run averages and therefore sell volatility.

When selling volatility, we have a couple strategy choices, namely selling straddles, strangles, iron condors, ratio spreads, butterflies, or credit spreads. Straddles, strangles, and ratio spreads are short more contracts than they are long and are currently out of reach for our account size. That leaves iron condors (ICs), butterflies/iron flies, and credit spreads. Flies are great when IV is high as ATM options have the highest vega in the chain, but consequently carry more gamma risk. Credit spreads are simple and neat but also inherently carry more delta exposure than I’d like to start off. That leaves us with the IC.

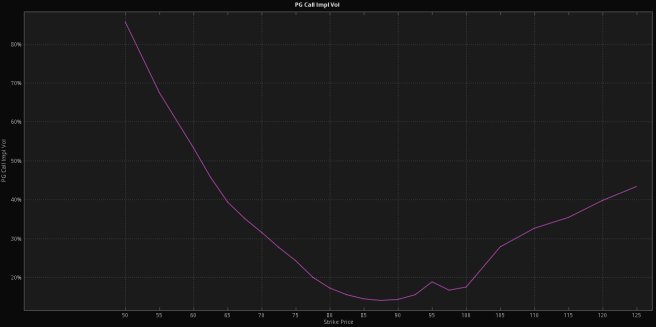

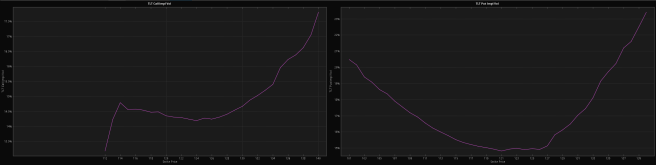

With our underlying and strategy selected, we can take a look at the volatility curve for calls and puts to help decide what strikes we want. With the ATM strikes being 120-121, we can see that ATM to near OTM volatility is fairly flat on the call side and sharper on the put side. Note how call IV doesn’t begin to ramp up until the $124 strike whereas put IV inflects ATM. This means the put strike selection will be more sensitive to volatility as we’ll be buying more volatility on the put side than call side, assuming we stay reasonably close to the money.

For the short strikes, I ended up choosing the closest to 30 delta, which were $117 and $124. This put me in a nice balance between taking in a decent credit and not having to pick long strikes that were too close in to avoid buying a lot of vol. On the long side I went with the $114 and $127 strikes, which happened to be in the 16-18 delta range. Any higher on the call side and I would have been buying a lot of vol, and much lower on the put side and I would have had too much long delta on.

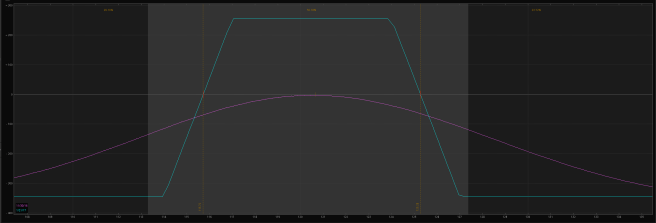

The executed trade payoff graph is shown below, where the blue line is payoff at expiry, the purple curved line is payoff right now, and the percent values at the top are probability zones. This graph can be made/found in the ToS Analyze tab.

That’s about it from start to finish. The GLD IC was put on with similar reasoning.

Today’s Trades (Greeks on Open):

- STO 1 Jan17 TLT 114/117/124/127 IC @ $1.27

- Delta: -0.36

- Gamma: -3.05

- Vega: -8.56

- Theta: 1.11

- STO 1 Jan17 GLD 103/106/118/121 IC @ $0.70

- Delta: -0.85

- Gamma: -2.68

- Vega: -7.01

- Theta: 0.95

The two trades have a combined buying power reduction (BPR) of $300 a piece, which is 12% of our account value per trade. This is higher than I’d like, but with a small account we’re in a tough place with putting on good trades while also keep our risk low.