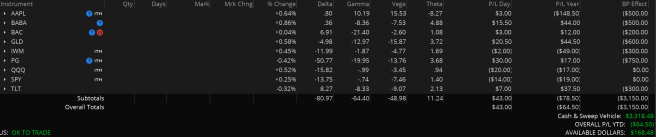

Week 5/Year 1 End NLV (AH): $2402.96 (-97.04/-3.88%)

The obligatory year end postmortem is upon us! Though our net liq (value above) shows us down 3.9 or so percent, it’s nice to see our overall YTD P/L +$43.00. I’m very proud of what we put together so far and excited to see what 2017 will hold. The positive P/L on the year is a nice icing on the cake for us moving forward. As the year is coming to end and our book is fairly well fleshed out at this point, I thought this would be a perfect time to reflect on what we’ve learned so far and map out our plan and goals for the coming year.

Lessons Learned

Two trading months aren’t much to start gleaning deep insight, but I believe we have learned a few things already. First off, and most obviously, was the catastrophic failure of the AAPL double calendar. In retrospect, I have no idea why I put on a calendar so far OTM. It was way too directional to be a straight vega play, and suffered even though IV shot from the 2nd to the 20th percentile in around a week. Had I placed it ATM we probably would have been at max profit today. Lesson learned.

The second lesson is that when placing defined risk trades, if we can’t afford to make the wings sufficiently wide, it might be best not to place the trade at all. On the BAC and PG spreads in particular, the tight wings give us a relatively narrow profit corridor. Apart from simple price dynamics, by buying tight wings we minimize the differential between the vega we’re buying (long strikes) and the vega we’re selling (short strikes). We should strive to come as close as we can to synthesizing strangles and straddles if that’s the type of volatility play we want to make.

The third lesson isn’t really a lesson, but more something I didn’t realize before. If we put on a defined risk trade such as an iron fly or condor, we enter the trade with very specific volatility assumption and risk tolerance. If we roll one side or the other, or adjust the legs, we change the risk profile of the trade. Should we treat this as a completely new trade? Should we take the old trade off and put an entirely new spread on instead? At what point (volatility or price move) should we start making these decisions? I honestly don’t know yet, but I’m going to get in the books soon and try and figure it out. If you have an idea, please leave a comment or drop me a line.

Looking Forward

In the year ahead, I have a single goal: to reach a net liquidating value of $5,000, which is double our starting capital. This milestone isn’t entirely arbitrary; it will open up futures options, the ability to trade naked options on cheaper instruments, and give us some opportunity to buy stock here and there. In addition, I want to stay focused on volatility plays and not stray away from our original rules. We simply don’t have enough capital to try and play big macro trends or stock direction and volatility at the same time in my opinion. For the time being, I’d also like to focus more on ETFs and indices than individual stocks to avoid earnings gap risks. In the upcoming earnings cycle I’m sure we’ll make an earnings play here and there but I forsee it difficult to apply our volatility trading techniques when gap risk is so significant as with earnings. Particularly with defined risk trades, you’re making a bet with unknown odds on either the stock staying within the implied move or blowing it out of the water one way or the other depending on how you play it. I’d rather sell iron condors on a bond ETF with high IV, but we’ll see. Money’s money.

Happy New Year, and Go Blue.