Week 5 NLV (AH): $2308.98 (-$191.02/-7.64%)

Today was the first trading session since the Christmas break and marks the start of the weird period between Christmas and New Year’s where trading gets very thin and big houses start to tidy up their books via position rebalancing, tax selling, etc. Since volumes will start to pick up again in early January leading into the next earnings season starting shortly thereafter, I decided to make some more adjustments today and deploy some dry powder on strategies with nearer than usual expirations. All in all five trades were made today: one roll, one to open, and three adjustments.

Two of those three adjustments were on the SPY and QQQ put debit spreads we opened last week. Price isn’t going where we need it to (down) and IV is ticking up a bit, leading to the spreads showing paper losses of around 10% each as of this morning and needing pretty significant down moves in the coming weeks, which is looking less likely than I originally thought. To take advantage of the recent creep upwards in IV and reduce the capital risk of the spreads, I sold the mirror image of the put spreads originally purchased — turning it into a butterfly, or “flying off” the spread. For the original SPY 223/228 put debit spread, this meant selling the 218/223 put spread for a credit of $0.78 to create a 218/223/228 put fly for a net debit of $1.27. For the QQQ 118/122 put debit spread, it meant selling the 114/118 put spread for a credit of $0.51, creating a 114/118/122 put fly for a net $1.08 debit.

Both of these trades, while not really my favorite way to adjust, raised our upside breakeven points, introduced a bit more short vega/long theta, and reduced our directional exposure (trading it for exposure to large downside moves).

Our other trades today were opening a short iron condor in PG (80/82.5/85/87.5) in the Jan’17 monthlies for $1.07 to offset some upside risk in our current iron fly, rolling down the BABA call half of our IC (again) to the 90/94 for $0.53 to flatten deltas, and selling the 111/114 call spread in GLD Jan monthlies for $0.49.

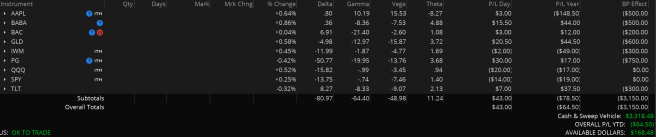

In the interest of brevity, here’s a snapshot of our current portfolio:

That dumb AAPL double calendar is still killing me and will likely be closed for near even (max loss) tomorrow unless I can pull off a fancy roll that moves it closer to the money without incurring any more margin or cost.