Week 4 NLV (Weds close): $2332.88 (-167.12/-6.7%)

More Delta Adjustments

Today’s U.S. session was extremely boring, which was a bummer since I didn’t have anything keeping me away from trading. Slow sessions can be nice since there’s no rush to get things done, but a three point range on the S&P until 3:30PM is like watching paint dry. Volatility across the board is still extremely depressed; in fact, the VIX hit the 10 handle this morning. Regardless, I made a few adjustments I thought I’d share.

If you’ll recall, a few weeks back we sold a GLD iron condor in the January ’17 monthlies for $0.70, with the short strikes near 20 delta. GLD IV — call IV in particular — has gotten smashed since we put the trade on, and the call half of the spread was trading for around a nickel. Being that cheap (and OTM), combined with the low IV, the call legs were contributing almost nothing to our position greeks. With only a few pennies left to make, all that was left was downside (i.e. capping profits to the upside). I also looked at rolling the spread down but unless I wanted to widen the strikes out and take on more risk, the credit was abysmal. I ended up getting the call spread off for $0.04 + commissions at around 10:00AM, leaving us with a 20 delta, $3 wide put credit spread for a net $0.64 less commissions (so probably $0.50 or so all said and done). Combined with our other GLD spread, our current position greeks are as follows:

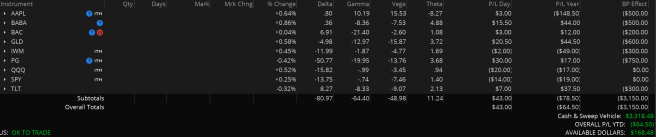

GLD Position Greeks: 18.14Δ, -8.39, -11.96ν, 2.00θ

A bit later I took a look at our TLT iron condor to make a delta adjustment, as it was getting a little heavy for my comfort. This spread was initially put on for a credit of $1.27, also with $3 wide wings. Unlike GLD, the TLT IC still had a little juice left in the call spread, so I decided to roll down as a straight delta adjustment, and was able to roll down to the 120/123 for a credit of $0.42, bringing our total credit for the position to $1.69 less commissions. I picked those strikes to bring the spread back close to 0 delta. At the time of the trade, the put legs of the IC had deltas of around 16 and 38, and the call legs we rolled into had deltas of 34 and 14.

TLT Position Greeks: 1.03Δ, -6.43γ, -9.15ν, 1.77θ

Dividend Risk

Overall though, today was pretty good P/L-wise, ending up about $52 on the day thanks to the Russell taking a dive in the last hour of trading. Speaking of which, tomorrow IWM goes ex-dividend, which is important for options traders. Any time you find yourself short calls on a stock or ETF that’s about to go ex-div, you’ve got exercise risk — that is, risk that the buyer of the call you sold will exercise in order to receive shares and therefore the dividend that comes with them. It’s crucial to determine how much risk your short calls have of being exercised — nothing’s worse than waking up and finding yourself short $80,000 worth of SPY on a $2,000 account. I know first hand, and it doesn’t end pretty…I was able to cover the position on open and only ended up eating $800, which sucks but is a lot less than $80,000!

Anyway, the main idea with dividend risk is that if the extrinsic value (time value premium) left in your calls is greater than the value of the dividend, you’re more than likely good to go. This makes sense intuitively if we use an example. Let’s say IWM is trading for $100 and you’re short a $99 call, which is currently trading for $3. Tomorrow’s dividend is $1. The person that bought that call has two options going into ex-div day: sell the call for $3 or exercise to buy 100 shares for $99 (netting $1/share if sold for $100 tomorrow) and receive a $1 dividend. Which would you pick, $3 or $2? The extrinsic value of the call here is $2, since it’s trading for $3 and $1 ITM.

In ToS, you can see how much extrinsic value an option has by adding it in your option chain settings, or simply taking the market value of the option and subtracting the amount by which it is in the money. In the case of our IWM IC, we’re short the $136 call, which closed around $2.71. Since IWM closed at $137, that means the call has (had) $1.69 of extrinsic value. The IWM dividend, from what I can find, will probably be no more than $0.70. Is the call an exercise risk?

Portfolio Greeks (AH, unweighted): -79.12Δ, -38.67γ, -27.62ν, 7.52θ